Milo Maltbie wrote

Z wrote

I like Bend a lot but it would be better for MC than me given it’s a very blue state

Eastern Oregon and Washington are not blue at all. It's not about the state. Rural areas are conservative and cities are liberal. Ski towns are mostly liberal in a libertarian kind of way. If the Dacks are too liberal for you, you'll probably need to move rural Idaho, or a ranch in the desert somewhere.

mm

MM is spot on here. I live in Eastern WA. If you exclude Seattle and Bellevue, it's pretty much a red state. It's mostly agriculture over here. Much of the conservatism is pretty traditional, as opposed to the propaganda driven bullshit that has infected our modern political reality. There is some Trumpism over here, but it's mainly found in the extreme rural areas.

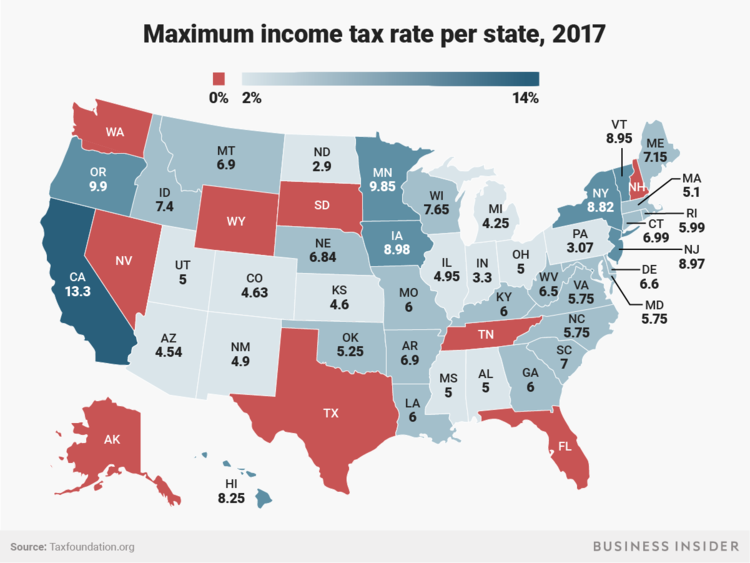

Z. I think you'd like it on this side of the Cascades. There is no state income tax, ultra-cheap electricity, and our property taxes are quite low. Legal weed has even lead to a couple of reductions over the past few years. I nearly fell over when I saw Jason's tax bill... I live in a fairly large house, and have never paid more than 4k annually. 15k seems almost unconstitutional.

Z. Off topic, but I'm curious, as I know you work in the medical device arena. I think you and I probably share a similar level of financial awareness. Perhaps this could be a good play for you. Over the past 6 moths or so, I have been trading Tandem Diabetes (TNDM). I was on a dive trip with one of their engineers back in January. She had many compelling stories about both their leadership team, and technology development process. Their new insulin pump looks to be far superior than anything currently in the pipeline. Initially, it was a high flyer, but faltered, and then screwed the pooch with a reverse-split back in late 2017. From a short-term perspective, it's been a fantastic play. I cashed out my entire position a few weeks ago, but saw that it's down 15% today. My research says long-term, it still looks pretty solid. I'm now considering going long on this. Any thoughts?